U.S. Home Prices Spiraling Out of Control

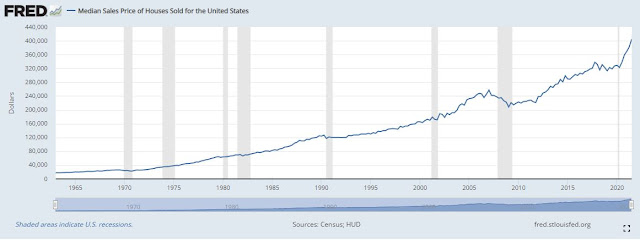

By Gary Halbert Between the Lines U.S. home prices soared by 18.4% in October alone over year-ago levels. That was actually slightly below the annual increase of 19.1% in September. Home prices are on fire, and no one knows how this unprecedented bull market will end. Here you can see what US home prices have done over the last 50+ years. The price rise has been spectacular, with no end in sight. Since the last low in 2010, median home prices have more than doubled from near $200,000 to above $400,000 today. The median home sale price in the US was $404,700 at the end of the 3Q. It is considerably higher in certain popular zip codes. Those would include Phoenix, Tampa and Miami just to name a few. Minneapolis and Chicago posted the smallest increases over the past year but still increased by 11.5%. The housing market has been strong thanks to rock-bottom mortgage rates, a limited supply of homes on the market and pent-up demand from consumers locked in last year by the pandemic. Many A...