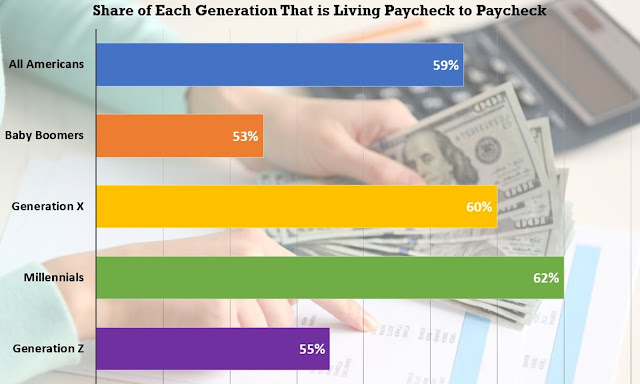

60% of millennials earning over $100,000 say they're living paycheck to paycheck

I always suspected that living paycheck to paycheck did not involve your income, but was influenced by bad behavior and outright ignorance of how to handle your personal finances. And throw in some vanity, and you've got a recipe for eating cat food in retirement. Or maybe you'd prefer dog food. Been there, done that, so I'll include myself in this category, until I shook off the insanity and put things right. I'm on a ribeye diet, nicely retired, thank you. Here are some facts, as reported by Business Insider. In a survey this June, 60% of millennials earning over $100,000 said they live paycheck to paycheck. Some of these millennials - known as HENRYs - prefer a comfortable, expensive lifestyle. In today's economy, $100,000 is considered middle class in the US. High-earning millennials feel broke. Sixty percent of millennials raking in over $100,000 a year said they're living paycheck to paycheck, found a survey this June by PYMNTS and LendingClub, which ana...