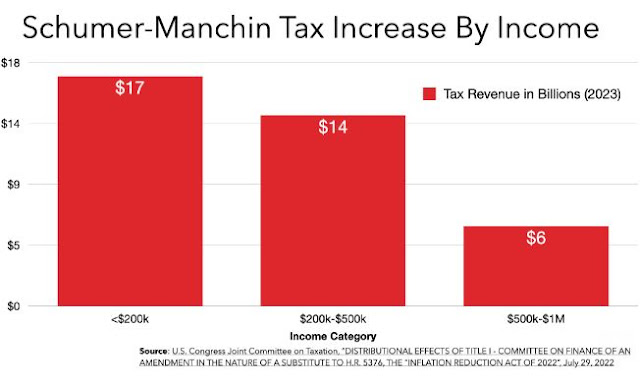

From the Tax Foundation. Full analysis here . Reconciling the reconciliation bill: The Inflation Reduction Act, successor to the House-passed Build Back Better Act of late 2021, has been touted by President Biden to, among other things, help reduce the country’s crippling inflation. Among the major tax changes are a 15 percent corporate minimum tax, drug price controls, IRS tax enforcement, and a tax hike on carried interest to pay for increased spending on energy and health insurance subsidies as well as deficit reduction. See a more comprehensive list here . According to our model, the bill would raise about $304 billion in net revenue from 2022 to 2031, but would do so in an economically inefficient manner, reducing long-run economic output by about 0.1 percent, eliminating about 30,000 full-time equivalent U.S. jobs, and reducing average after-tax incomes for taxpayers across every income group in the long run. What about inflation? On balance, the long-run impact on inflation...

.png)